Please refer to Accounting for Partnership Firms – Basic Concepts Class 12 Accountancy Important Questions with solutions provided below. These questions and answers have been provided for Class 12 Accountancy based on the latest syllabus and examination guidelines issued by CBSE, NCERT, and KVS. Students should learn these problem solutions as it will help them to gain more marks in examinations. We have provided Important Questions for Class 12 Accountancy for all chapters in your book. These Board exam questions have been designed by expert teachers of Standard 12.

Class 12 Accountancy Important Questions Accounting for Partnership Firms – Basic Concepts

Question. Chandar and Suman are partners in a firm without a partnership deed. Chandar’s capital is Rs. 10,000 and Suman’s capital is Rs. 14,000. Chander has advanced a loan of Rs. 5000 and claim interest @ 12% p.a. State whether his claim is valid or not.

Answer : Chander’s claim is not valid as in the absence of partnership deed interest on partners loan is provided @ 6% p.a.

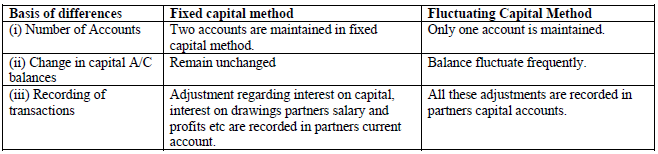

Question. Distinguish between fixed capital method and fluctuating capital method.

Answer : Distinction between Fixed and Fluctuating Capital method:-

Question. A, B and C are partners in a firm, B withdrew Rs. 800 at the end of each month of the year. Calculate interest on B’s drawings @ 6% p.a.

Answer : Interest on drawing = 9600 X 6/100 X 5.5/12 = 264

Question. A and B are partners sharing profits in proportion of 3:2 with capitals of Rs. 40,000 and Rs. 30,000 respectively. Interest on capital is agreed at 5 % p.a. B is to be allowed an annual salary of Rs. 3000 which has not been withdrawn. During 2001 the profits for the year prior to calculation of interest on capital but after charging B’s salary amounted to Rs. 12,000. A provision of 5% of this amount is to be made in respect of commission to the manager.

Prepare profit and loss appropriation account showing the allocation of profits.

Answer : 15 Net profit transferred to A’s Capital A/C Rs. 4,650

B’s Capital A/C Rs. 3,100

Question. Alka, Barkha and Charu are partners in a firm having no partnership agreement. Alka, Barkha and Charu contributed Rs. 20,000, Rs. 30,000 and Rs. 1,00,000 respectively. Alka and Barkha desire that the profit should be divided in the ratio of capital contribution. Charu does not agree to this. How will you settle the dispute.

Answer : Charu is correct as in the absence of partnership agreement, profits and losses are divided equally among partners.

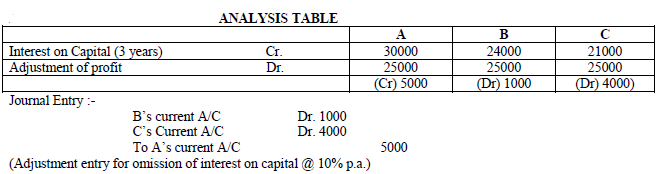

Question. A, B and C are partners in a firm. They have omitted interest on capital @ 10 % p.a. for three years ended 31st march 2007. Their fixed capitals on which interest was to be calculated through –out were

A Rs. 1,00,000

B Rs. 80,000

C Rs. 70,000

Give the necessary Journal entry with working notes.

Answer :

Question. R, S, and T entered into a partnership of manufacturing and distributing educational CD’s on April 01, 2006. Rlooked after the business development, S content development and T financed the project. At the end of the year (31-03-2007) T wanted an interest of 12% on the capital employed by him. The other partners were not inclined to this. How would you resolve this within the ambit of the Indian Partnership Act, 1932?

Answer : As per provision of Indian Partnership act 1932, when there is no partnership, no partner is entitled for interest on his capital contribution.

Question. A is partner in a firm. His capital as on Jan 01, 2007 was Rs. 60,000. He introduced additional capital of Rs. 20000 on Oct 01 2007. Calculate interest on A’s capital @ 9% p.a.

Answer :

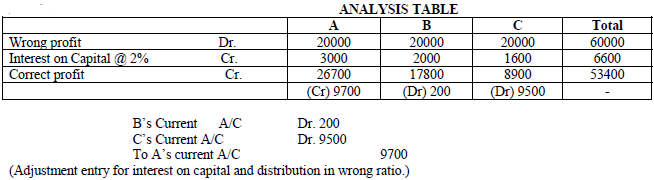

Question. A, B and C are partners sharing profits and losses in the ratio of 3:2:1. Their fixed capitals are Rs. 1,50,000, Rs. 1,00,000 and Rs. 80,000 respectively. Profit for the year after providing interest on capital was Rs. 60,000, which was wrongly transferred to partners equally. After distribution of profit it was found that interest on capital provided to them @ 10% instead of 12% . Pass necessary adjustment entry.

Show your working clearly.

Answer :

Question. A and B are partners in a firm without a partnership deed. A is an active partner and claims a salary of Rs. 18,000 per month. State with reason whether the claim is valid or not.

Answer : A’s claim is not valid as in the absence of partnership deed, no salary is allowed to partners.

Question. A, B and C were partners in a firm having capitals of Rs. 60,000, Rs. 60,000 and Rs. 80,000 respectively. Their current account balances were A- Rs. 10,000, B- Rs. 5000 and C- Rs. 2000 (Dr.). According to the partnership deed the partners were entitled to an interest on capital @ 5% p.a. C being the working partner was also entitled to a salary of Rs. 6,000 p. a. The profits were to be divided as follows:

(i) The first Rs. 20,000 in proportion to their capitals.

(ii) Next Rs. 30,000 in the ratio of 5:3:2.

(iii) Remaining profits to be shared equally.

During the year the firm made a profit of Rs. 1,56,000 before charging any of the above items.

Prepare the profit and loss appropriate on A/C.

Answer : Profit transferred to A’s current A/C Rs. 51,000

B’s current A/C Rs. 45,000

C’s current A/C Rs. 44,000

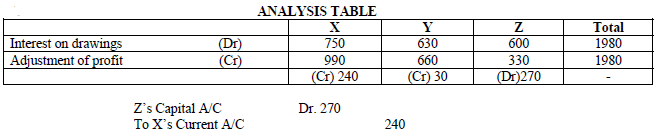

Question. X, Y, and Z are partners sharing profits and losses in the ratio of 3:2:1. After the final accounts have been prepared it was discovered that interest on drawings @ 5 % had not been taken into consideration. The drawings of the partner were X Rs. 15000, Y Rs. 12,600, Z Rs. 12,000. Give the necessary adjusting Journal entry.

Answer :

To Y’s current A/C 30

(Adjustment entry for omission of interest on drawings @ 5 % p.a.)

Question. A, B and C are partners in a firm. A withdrew Rs. 1000 in the beginning of each month of the year. Calculate

interest on A’s drawing @ 6% p.a.

Answer : Interest on drawing = 12000 X 6/100 X 6.5/12 = 390

Question. State the conditions under which capital balances may change under the system of a Fixed Capital Account.

Answer : (i) When additional capital is introduced.

(ii) When capital is withdrawn.

Question. Ravi and Mohan were partner in a firm sharing profits in the ratio of 7:5. Their respective fixed capitals were Ravi Rs. 10,00,000 and Mohan Rs. 7,00,000. The partnership deed provided for the following:-

(i) Interest on capital @ 12% p.a.

(ii) Ravi’s salary Rs. 6000 per month and Mohan’s salary Rs. 60000 per year.

The profit for the year ended 31-03-2007 was Rs. 5,04,000 which was distributed equally without providing for the above. Pass an adjustment Entry.

Answer :